The financial markets took a big dip early this week over fears about the spreading coronavirus, erasing gains from earlier this year. After the Dow lost over 800 points on Tuesday, it was down a total of 1,900 points in two days.

Investors are understandably nervous about their money and their health. If you are worried about your portfolio, you’re not alone. But during stock market volatility, it’s important to keep a level head to avoid financial mistakes.

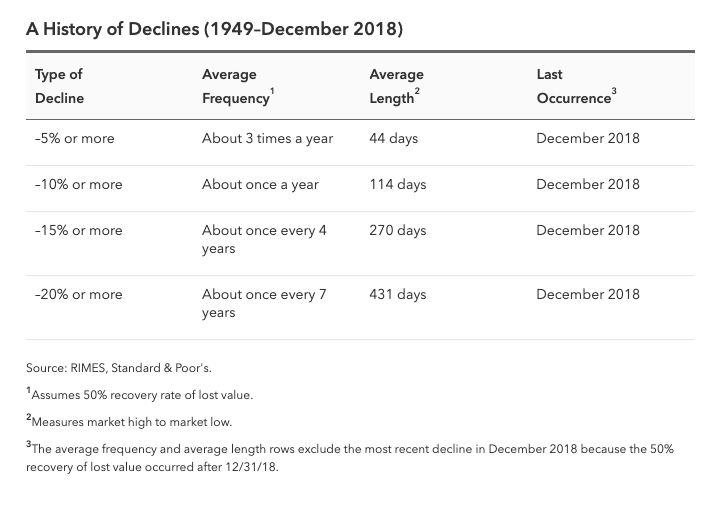

Stay Calm

At times like these, it’s important to put current conditions into perspective. This is not the first time the market has taken a tumble and it won’t be the last. Declines in the Dow Jones Industrial Average are actually fairly regular events. In fact, drops of 10% or more happen about once a year on average.

Keep An Eye On The Situation

We simply do not have enough information yet to know how the coronavirus will impact the economy in the short and long term. It’s possible that the virus will soon be well-contained and the markets will recover. But it is also possible that the virus will spread and impact global markets, which would lead to a full correction or even a longer-term recession.

It’s important to remember that markets dislike uncertainty. With so much uncertainty over how fast the virus could spread and the potential impacts, volatility right now is extreme. As we get more information, it is likely that day-to-day market fluctuations will decrease.

Play Dead

There’s an old saying that the best thing to do when you meet a bear market is the same as if you were to meet a bear in the woods: play dead. While easier said than done, successful long-term investors know that it’s important to stay calm during a market correction. We don’t know yet whether the coronavirus fears will translate into an official correction, but the risk always exists.

Market volatility has increased in recent years and the media can often make it seem like each episode is worse than the one before. In reality, volatility does not hurt investors, but selling when the market is down will lock in losses.

Remember That Your Portfolio is Diversified

We understand that volatility and market declines are stressful. However, we encourage you to keep in mind that while the stock market may be down significantly, your portfolio is made up of both stocks, bonds, and other assets that are designed to work together to decrease overall losses. It’s important to consider your specific portfolio, investment horizon, and circumstances when reflecting on economic events. If you have questions about your portfolio, get in touch with our office.

Review Your 401(k) and Other Accounts

Now is a good time to take a look at all of your investment accounts, including your 401(k) to make sure it is well-diversified. If you have not reviewed the investment accounts that we do not manage, get in touch with our office and we’ll take a look and offer recommendations to minimize potential losses.

Speak With Your Advisor

Whether you’re new to investing or an experienced investor, it’s helpful to consult with an objective third party. Human nature causes us all to act out of emotion when our accounts go down. As an independent firm, we put your best interests first. We seek to serve as a support system for our clients, helping them make informed financial decisions that aren’t driven solely by emotion.

We’re Here for Your Friends and Family

If you have friends or family who need help with their investments, we are happy to offer a complimentary portfolio review and recommendations. We can discuss what is appropriate for their immediate needs and long-term objectives. Sometimes, simply speaking with a financial advisor may help investors feel more confident and less concerned with the day-to-day market activity.