Did you know that four in ten Americans admit that they prefer not to think about money? (1) This isn’t all too surprising as, for many people, finances can seem complicated and overwhelming, and many people suffer from decision fatigue and don’t know where to start. If that’s you, take a look at these five steps to get your financial house in order.

1. Gather and Organize Your Financial Documents

Despite how digital our lives are becoming, there are still times we need physical documents. Find a system that works for you, whether it’s a binder, a locked filing cabinet, or an in-home, fireproof safe.

To start, separate your financial papers into three categories: bills, documents or statements to save, and old items you can toss. Gather everything together neatly and store it in one place that is easy for you to access.

Utilize a Password Manager Tool

Do you have a system for keeping track of your countless usernames and passwords? You’ll save yourself some headaches if you can find a method to keep all your information in one place. There are plenty of online password managers to choose from, but however you decide to organize your login details, be sure to regularly update your passwords to protect yourself from hackers.

Go Green

If you want to minimize the amount of paper that piles up on your counters, save a tree and get rid of clutter by enrolling in paperless document delivery for all your bills and financial services. Since you’re planning to create a password management strategy, the only thing you’ll need to do to access account details is find your login information and be on your way.

Communicate

Develop a master directory that lays out all your financial information to help you manage your affairs and serve as a guide to your family members if they ever need to assist with your finances. Be sure to include account numbers and logins and keep this document password-protected or under lock and key.

2. Set and Follow a Budget

Part of being financially organized includes being aware. If you know how much money is going in and out and stick to a budget, you won’t find yourself scrambling to pay bills or wondering where that recent paycheck went.

A budget helps you establish parameters for operating your household, understand if your goals are achievable in your desired timeframe, and may help reduce stress in the event of an unexpected incident, such as the loss of a job or an injury.

3. Automate Everything

Automating your bills and savings not only streamlines and organizes your life, but also has long-term benefits for your financial world. Paying your bills automatically tends to improve your credit score, makes budgeting simpler, and can also make income tax preparation easier.

Additionally, by automating your savings, you give yourself a chance to save before you can even touch the money.

4. Tackle Your Debts

If you are excited about conquering your goals, one of the first steps you need to take is to eliminate debt. When you are paying 10-30% interest on any number of credit cards or loans, you are cutting down on the money you have available to put towards your goals.

Become relentless about reducing your debt and interest costs and consolidate accounts where you can. If you have a loan with a significantly higher interest rate than the others, you may want to work on paying off that one first. Or, if you’re feeling overwhelmed by debt, try paying off the loan with the smallest balance first, no matter the interest rate, in order to gain some momentum.

An emergency fund can help you avoid accumulating more debt. By creating a liquid, easily accessible savings account, you won’t have to rely on debt to cover those inevitable life expenses, such as home repairs or medical bills. Create this cash cushion by putting aside money from each paycheck until you have enough to cover approximately three to six months worth of living expenses. You will never regret having an emergency fund at the ready.

5. Create or Update Your Will

It’s estimated that nearly 70% of Americans die without a will. People may avoid completing their wills because they don’t like to acknowledge that they will die or they may think it’s a complicated and expensive process. But the truth is that the value for your loved ones and heirs will far exceed your cost and effort. In the simplest of terms, a will allows you to ensure that you can leave a legacy to your desired beneficiaries, from physical household items to assets. Without a will, the state will determine what will happen to your assets and the process for your survivors and heirs may be much more complicated and time-consuming than it should be.

If you don’t already have a will, it’s time to work with an experienced professional to create one. If you haven’t reviewed yours in five or more years, it’s time to review and make any necessary updates.

Ready To Get Started?

Working with a financial planner involves more than just opening an IRA and setting up monthly contributions. Advisors add value to your money and your life by taking care of the details and giving you confidence in your financial future. If you want to benefit from the knowledge and experience of a financial planner as you get your financial house in order, give me a call at 949-445-1465 or email me at jgilbert@balboawealth.com to schedule a meeting.

About Jeff

Jeff Gilbert is the founder and CEO of Balboa Wealth Partners, a holistic financial management firm dedicated to providing clients guidance today for tomorrow’s success. With nearly three decades of industry experience, he has worked as both an advisor and executive level manager, partnering with and serving a diverse range of clients. Specializing in serving high and ultra-high net worth families, Jeff aims to help clients achieve their short-term and long-term goals and to worry less about their finances and more on their passions in life. Based in Orange County, he works with clients throughout Southern California, as well as Arizona, Oregon, and Washington. To learn more, connect with Jeff on LinkedIn or email jgilbert@balboawealth.com.

Advisory services offered through Balboa Wealth Partners, Inc. An SEC registered Investment Adviser. Securities offered through Chalice Capital Partners, LLC, member FINRA, SIPC

Balboa offers advisory services independent of Chalice. Neither firm is affiliated.

_________

(1) https://files.consumerfinance.gov/f/cfpb_fin-ed-digest_organizing-finances.pdf

The closer you get to retirement, the more excited you probably get. It’s a milestone we often start thinking about as soon as we enter our working years, and many of us relish the idea of slowing down, changing pace, and finally having all the time we need to pursue passions and invest in relationships. But what happens when you get to retirement and it’s not all it’s cracked up to be? Have you considered the idea that you could regret your decision to retire? Here are four common retirement regrets to keep in mind as you prepare for your golden years.

1. Retiring Too Soon

Whether you were forced to retire earlier than planned or you made the decision on your own, retiring before you are ready can cause plenty of regret. In fact, 30% of retirees admitted they would gladly re-enter the workforce if a job became available. (1)

If you decided to retire prior to turning 65, you probably had to find pre-Medicare coverage, which is often quite a bit more expensive than an employer-sponsored plan. By waiting until you turn 65, you will qualify for Medicare and not be forced to obtain other health insurance to cover you during the transition.

Financially, the earlier you retire the fewer years you have to save and the longer you will have to live off of your money. If your finances are keeping you up at night or you are living at a lower quality of life than you are used to, you may regret retiring when you did.

Working even a few years longer can provide these valuable benefits:

- More time to accumulate savings

- More years to apply towards Social Security which could result in a larger benefit amount

- Health insurance coverage through your employer

- Purpose and identity

- Stronger mental and physical health (2)

2. Not Creating a Social Security Claiming Strategy

Social Security benefits can be claimed anytime between ages 62 and 70. However, the timing of when you choose to collect these benefits will impact the amount of benefit you receive.

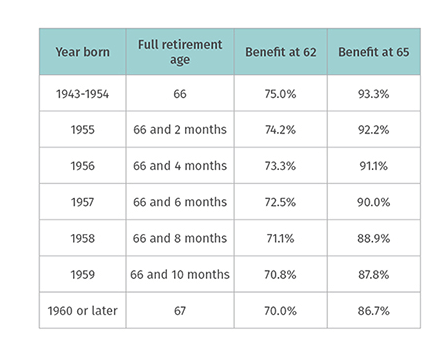

Full retirement age (FRA) changes based on the year you were born. For those born in 1937 and earlier, FRA is 65. After 1937, two months is added each year until FRA becomes 66 for those born between 1943 and 1954. Starting in 1955, two months a year is added again until the FRA becomes 67 for those born in 1960 or later.

If you wait until you reach full retirement age to begin collecting your Social Security benefits, you will receive your full Primary Insurance Amount, which is the full benefit that you have earned, but if you choose or are forced into an early retirement, you will receive a reduced benefit. Your basic benefit is reduced a fraction of a percent for each month you begin receiving benefits prior to full retirement age, up to 30%.

3. Overspending in the First Years of Retirement

Even if you have a solid nest egg saved to carry you through retirement, you still need to exercise financial discipline to ensure your money lasts. Dipping too deep into your savings as soon as you retire could make or break your retirement dreams. Instead, create a realistic retirement budget, factoring in travel or hobbies, then work with your advisor to find a withdrawal rate that will stretch your money for as long as possible.

4. Not Having a Retirement Bucket List

Free time is a major perk of retirement, but when you go from working full-time to not working at all it can be a shock to your system. Saying goodbye to your career, your colleagues, and your routines can cause anxiety and depression. But if you plan ahead to fill your time with activities that will fulfill you, you can avoid the negative emotions that can come with this life transition.

Do you want to know what activities result in a fulfilling retirement? A BMO study on retirement planning reveals that retirees who stayed busy and active, pursued independence, and volunteered their time were satisfied with their life. (3) One study of retirees even found that those who volunteered 200 hours a year were less likely to develop high blood pressure. (4) The takeaway here is to be intentional about your time in retirement. Make a list of things you want to do, places you want to go, and people you want to spend time with, then strategically map out the details so your goals become a reality. It’s easy to lose your identity when you say goodbye to your career, but filling your time and venturing out into new territory will help you build a new identity and give you something to look forward to.

Live With No Regrets

You probably don’t want to celebrate the incredible milestone of retirement and then wake up the next day wondering if you made the right decision. Deciding when and how to retire is one of the most difficult decisions you will make in life, but you don’t have to make the hard choices alone. If you want to avoid facing these common regrets when you retire, reach out to us for a no-obligation conversation by calling 949-445-1465 or emailing jgilbert@balboawealth.com.

About Jeff

Jeff Gilbert is the founder and CEO of Balboa Wealth Partners, a holistic financial management firm dedicated to providing clients guidance today for tomorrow’s success. With nearly three decades of industry experience, he has worked as both an advisor and executive level manager, partnering with and serving a diverse range of clients. Specializing in serving high and ultra-high net worth families, Jeff aims to help clients achieve their short-term and long-term goals and to worry less about their finances and more on their passions in life. Based in Orange County, he works with clients throughout Southern California, as well as Arizona, Oregon, and Washington. To learn more, connect with Jeff on LinkedIn or email jgilbert@balboawealth.com.

_________

(1) https://www.cnbc.com/2014/08/21/retirees-go-back-to-work.html

(2) http://www.medicaldaily.com/planning-retiring-early-consider-these-5-health-risks-first-247669

(3) https://commercial.bmoharris.com/resource/wealth-management/whats-your-retirement-game-plan/

(4) http://psycnet.apa.org/journals/pag/28/2/578/?_ga=1.177767717.1281536077.1488342343